Along with other retirement accounts and life insurance, savings bonds are often considered “non-probate assets,” meaning that they are not typically bequeathed in accordance with a person’s will. Instead, many times, they are “payable upon death” to the person(s) (or entity, such as a trust) that had been designated as the co-owner or beneficiary. (This is why keeping beneficiary designations current is highly critical! Leave your ex-spouse in the beneficiary box and, well, it belongs to them regardless of how the remainder of your assets have been appropriated!)

Things become more complicated when no survivor is named or that person has passed away. In that case, the bond becomes an asset of the estate and distribution can take months or even years.

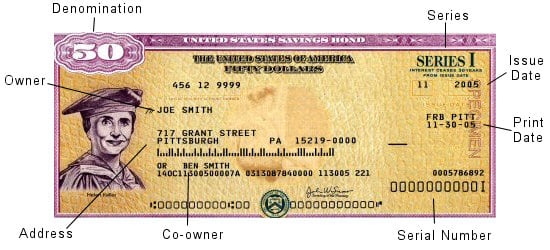

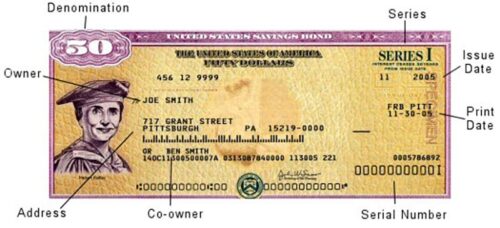

Inheriting Savings Bonds

If you inherit a savings bond, the first step is to determine the value and interest being earned (if any). Bonds first started being issued electronically in 2002, allowing owners to check the value of the holdings online. To check the value of older bonds, you can visit the U.S. Department of the Treasury’s Savings Bond Calculator.

Once you have determined the value, interest rate and maturity date, you have the option to either cash it out or have it reissued in your name. Before making this decision, it’s important to understand the administrative requirements and the income tax considerations.

- It, of course, makes sense to cash out bonds that have matured and therefore stopped earning interest.

- If the bond is still accruing interest, however, it may make sense to hold onto it. Depending on the type of bond and when it was issued, the interest rate could be significantly higher than that other of other low-risk investments like Treasury bills, CODs, and money market funds.

- Most people choose to defer or delay paying income tax on the interest earned by their savings bonds. [the other choice is to pay the income tax on the interest each year, even though the interest is not received until the bond is redeemed]. As a result, when inheritors redeem inherited bonds on which the tax has been deferred, they will owe tax on all the interest that has accumulated.

- If you choose to have a bond reissued, you have the option of paying tax on the interest accumulated up until the original bondholder's date of death, and then either accruing or deferring any subsequent tax.

- Another option is that the interest accumulated up until the original bondholder’s date of death can be reported on the original bondholder’s final income tax return. In some situations, that can actually reduce the income tax burden, though it may be paid by someone other than the person receiving the bond.

- If there is no named beneficiary of the bond, then it will be distributed according to the bondholder’s estate and Will. Then, if you decide on having the bond reissued prior to the settling of the estate, it is possible to have the tax on the accumulated interest paid directly by the estate, rather than coming out of your own pocket.

- Whoever does end up paying the income tax on a particular bond, whether it’s the estate or the beneficiary, is entitled to a tax deduction for the portion of the Federal estate tax attributable to the interest on the inherited bonds. Please note that only estates in excess of $5,430,000 will pay any Federal estate tax.

- If you choose to have the bond reissued and then defer future tax, it is important to maintain records of what income tax has already been paid. Otherwise, years from now when the bond matures or is redeemed, you or your beneficiaries could wind up paying too much in taxes.

How to Avoid Paying Taxes on Savings Bonds

The Education Tax Exclusion

The IRS lets you avoid paying taxes on interest earned by Series EE and Series I savings bonds when you redeem them if you use the money toward qualified higher education costs for yourself, your spouse, or any of your dependents.

To discuss making updates to your beneficiary designations, or for help with an inherited non-probate asset, please contact Altman & Associates.